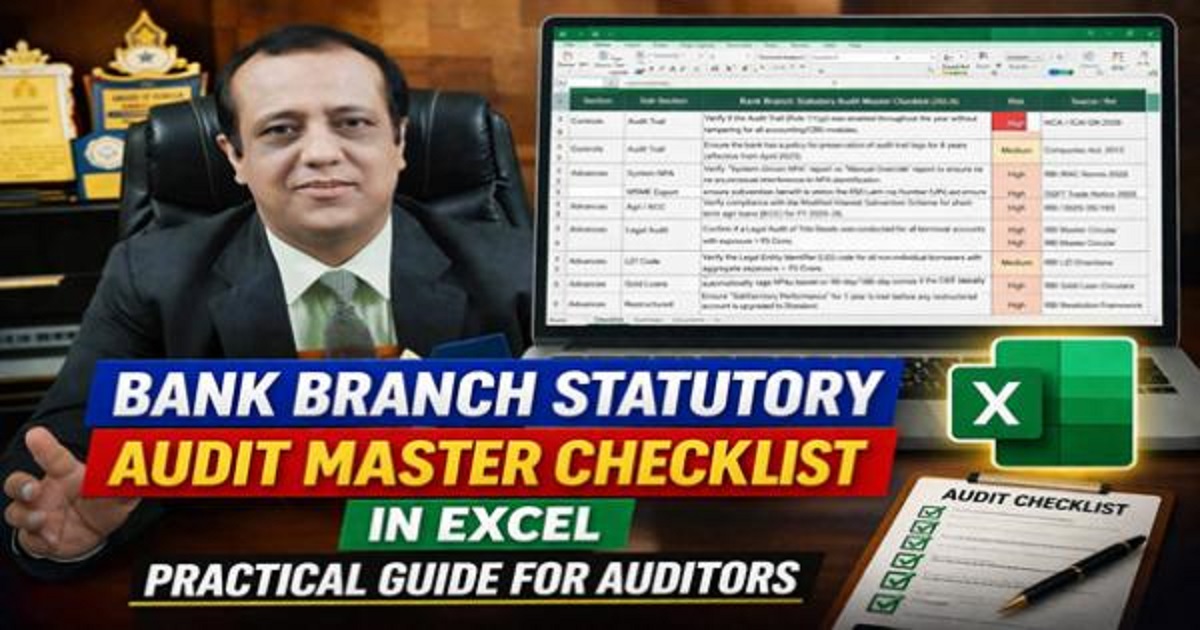

Asser Allocation Guide for Retired Senior Citizens

Today’s senior citizen has many more challenges to face than in days past e.g. the increasing inflation and healthcare costs. They also have to look at the threat of capital erosion and fluctuating interest rates. With smart planning an older couple/individual can manage the above concerns and other key aspects that one needs to consider during retirement years.

Following is a general guide on asset allocation for retirees.

Allocate 60-65% of portfolio in Fixed Income products; this will offer maximum safety and stable returns from your invested money. This is your best bet for regular income. Such income can be used to provide for monthly expenses, channel it to a recurring deposit account, and/or meet non-discretionary expenses (such as annual maintenance of house, buying presents for loved ones during festivals and celebrations, pilgrimage visits, etc.).

Form of investment - bank term deposits, government savings schemes, immediate Annuity Pension Plans (for example, LIC’s New Jeevan Akshay and HDFC Immediate Annuity), debt mutual funds and long-term bonds (such as Infrastructure bonds, RBI Relief bonds, etc.).

![]() Investments in Equity mutual funds (15-20%) will allow superior returns necessary for growth of your portfolio.

Investments in Equity mutual funds (15-20%) will allow superior returns necessary for growth of your portfolio.

Form of investment - large-cap Equity Diversified Mutual funds, Equity-linked Saving Schemes (ELSS), and Index funds/Index ETFs.

![]() Gold will provide to your portfolio the required hedge against the inflation monster. However, ensure maximum investment of 5-10% of your portfolio.

Gold will provide to your portfolio the required hedge against the inflation monster. However, ensure maximum investment of 5-10% of your portfolio.

Form of investment - physical gold (jewellery, gold bars and coins), gold Exchange Traded Funds (ETFs) and gold mutual funds.

![]() Real Estate offers the security of owning a house, regular income (in the form of rents) and capital appreciation in the long term, although it is advised not to go overboard with real estate due to its illiquid nature.

Real Estate offers the security of owning a house, regular income (in the form of rents) and capital appreciation in the long term, although it is advised not to go overboard with real estate due to its illiquid nature.

Form of investment – residential/commercial property, plot of land or real estate mutual fund schemes.

![]() Hold 15-20% of your portfolio as Cash to meet any sudden emergencies.

Hold 15-20% of your portfolio as Cash to meet any sudden emergencies.

Form of investment - Bank savings account, Bank multi-deposit savings account, Liquid mutual fund schemes and Short-term bond mutual fund schemes.

Note: The above asset allocation for retirees is a general guide and circumstances may vary from individual to individual. It is advisable to take the services of a Certified Financial Planner for customised financial planning. You may do this with InvestmentYogi’s Financial Planner.

Category : Finance | Comments : 0 | Hits : 1705

Comments